Photo: The Neighborhood Developers

So this pile of boxes won a big prize. Well, this and a few other components in the redevelopment of the old Box District in Chelsea, Mass. Together they won the Jack Kemp Award for Excellence in Affordable Housing. Yay. Nothing wrong with that.

But how do we feel about the way this looks?

Architecture is doing this now–boxes. All over Munjoy Hill, and now in the West End.

Of course, nothing in the world makes more sense than a flat roof–if it’s covered with plants and/or solar panels. On the other hand, New England’s history is one long tale of pitched roofs. On occasion, an Italianate bay window elbowed its between the typically flat and somber facades. Clapboard, shingle, and brick were the only sidings a respectable Pilgrim would consider.

Change happens, however. This award-winning development is platinum LEED certified, efficient, and even located on a mass-transit line, which is fantastic. The larger project revitalized what was formerly the neglected grave of a cardboard box factory. Yay.

![Glickman%20Library[1]](https://geekrealtyblog.com/wp-content/uploads/2014/10/glickman20library1.jpg?w=300&h=133)

Photo: USM

I’m just not sure I understand what this design is talking about. What is it saying to the buildings around it, to the ground beneath it, to the climate overhead? Housing design, like clothing and hair styles, is subject to fads. Some styles age better than others. How will the Box Era be judged in the coming decades?

In defense of the Box, I felt certain when the USM library got its

Photo: 118 on Munjoy Hill

makeover that God would smite it from the face of the earth, and that has not happened. Has it aged well? I don’t know. Maybe it’s acquired the sort of patina a cardboard box gets after a winter outdoors.

But this Munjoy Hill design, in a neighborhood of restrained and Pilgrimmy buildings: In 20 years, will this blend in? Or will anyone care?

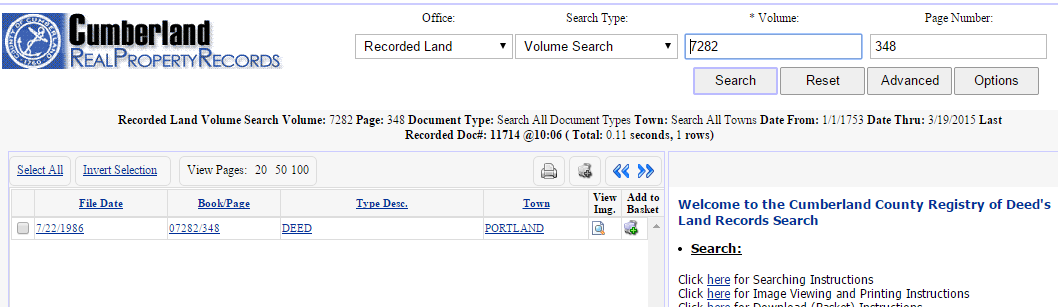

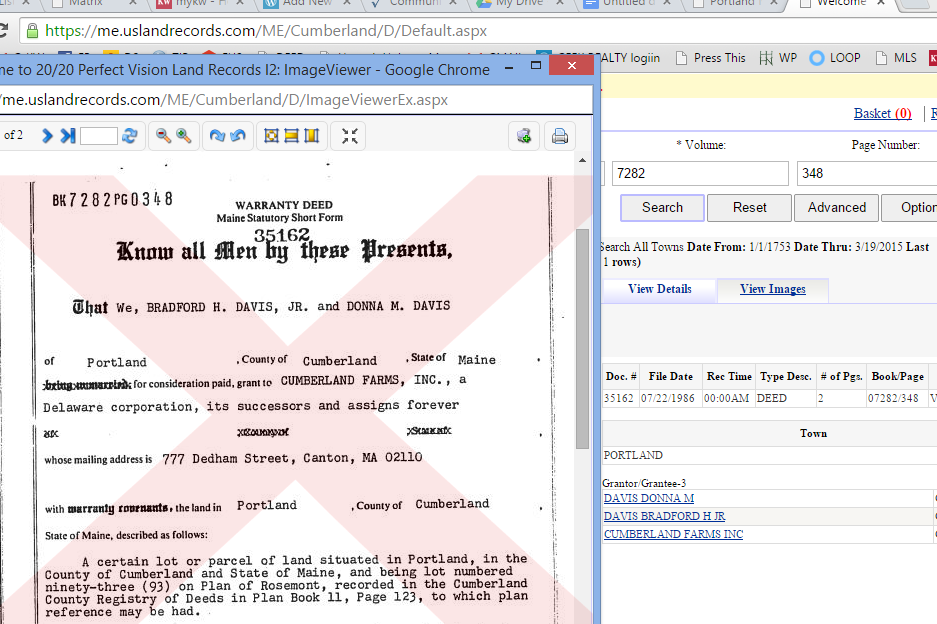

numbers from the card. We’re going to find the deed for this property at the Registry of Deeds. Here’s

numbers from the card. We’re going to find the deed for this property at the Registry of Deeds. Here’s

![Wikimedia [PD]](https://geekrealtyblog.com/wp-content/uploads/2015/03/pieter_willem_frederick_wenning_south_african_1873-1921_narrow_street_malay_quarter_cape_town.jpg)