Link out to this fun piece on Maine’s

Link out to this fun piece on Maine’s old antique vintage legacy venerable housing stock — and how to buy without getting burned.

Tag Archives: house

SEWAGEFUNGUS: NOT A SELLING POINT

There have been fewer foreclosed houses on the market lately, so when one popped into the MLS today I popped over to take a peek. Emphasis on pee. Or puke: I popped over to take a puke.

There have been fewer foreclosed houses on the market lately, so when one popped into the MLS today I popped over to take a peek. Emphasis on pee. Or puke: I popped over to take a puke.

Here’s some frustrating background: It takes an average of 600-plus days to foreclose a house. And a whole lot of sh*t can happen in 600 days. Especially if the occupant goes away mad on Day 242 without draining the pipes.

So, in my experience, most foreclosed homes have been through a winter of frozen pipes, and a springtime of indoor flooding. The furnace is often defunct from flooding, freezing, or both. The baseboard pipes may be split in a number of secret locations to be revealed only when the new owner opens a new account with the Portland Water District. The wood floors are buckled; the stench of mold and heartbreak hangs thick in the air.

(In the best cases, the bank that now owns the house has hired someone to drain the pipes, dump antifreeze in the toilet, and return every few months to pull the pin on a Glade grenade the size of a pineapple. I actually prefer the scent of sewagefungus.)

Anyway, foreclosure often sets water free, and free-range water is almost never helpful to the inside of a house. Mold happens. If sewage is stuck somewhere when frost sets in, that too can spread a fantastic feast for fungi. Today’s house had that scent — sewagemold plus heating oil.

People are increasingly freaky about bunking with mold, our species’ cave-sleeping past notwithstanding. Aint no bank gonna lend normal people money to buy a mold house. The only person equipped to purchase a fungusy foreclosed house is generally a renovator. A flipper. A professional fungus jockey.

And so today’s foreclosure, which I had hoped might fit my artistic and modestly-budgeted clients, was a disappointment. The burgundy shag on the stairs they could handle. The blue bathroom they could manage. But mold won’t fly. A Glade bomb had been detonated, but it came nowhere near drowning the smell of waste and heartache.

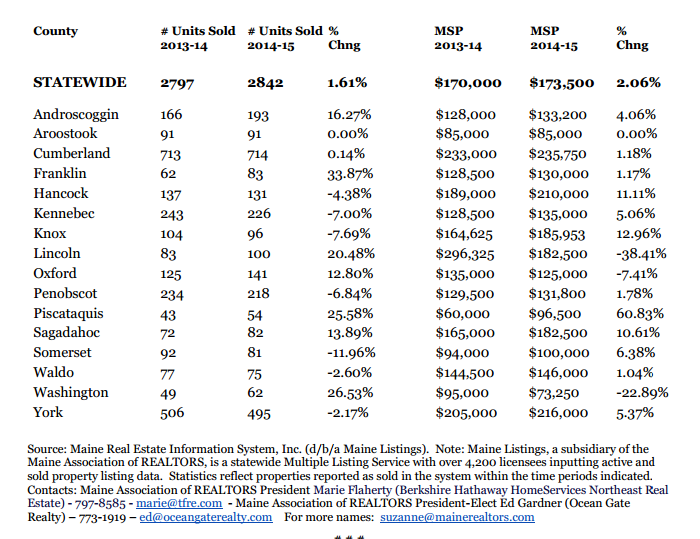

JANUARY REAL ESTATE STATISTICS IN MAINE

JANUARY THAW?

Weird, still weird in Maine: not enough houses where people want them (intown Portland, pretty much, or a second home on water); and too many, faaaaaar too many, in much of the remaining acreage of this post-industrial landscape.

I often wish it were easier to slide houses around, or helivac them to where they’re wanted. Whenever we visit my inlaws in Glens Falls, NY, I get misty about the fabulous old Victorians, Greek Revivals, Brick Behemoths, and Umpteen-Gabled Bungalows. Many of them are empty, crumbling, bed sheets across the windows. If they were in Portland, they’d be inhabited, and adored.

People used to move houses a lot more than they do now, by ice or water, or ox-team. Now that houses are quicker to build and expensiver to move, we’ve kind of quit.

Since humans left home, our species has faced this problem. We’re restless by necessity. We must follow food, whether it’s in the form of wildlife or jobs. If our shelters can’t be rolled up and dragged along, they must be left behind.

The abandoned and unloved houses haunt me. They were built to solve an urgent human problem, and often the artistic ideals of the builders were recorded in the process–as were the additions and subtractions of future inhabitants. And then they’re left, these rooted, semi-living things, to die.

Pretty philosophical, for a sheet of number, perhaps. I plead extenuating circumstances.

PEOPLE WHO OWN GREEN HOMES DESERVE BETTER CREDIT SCORES

![Honey, what's our credit score? [PD]Wikimedia](https://geekrealtyblog.com/wp-content/uploads/2015/01/agostino_brunias_-_a_leeward_islands_carib_family_outside_a_hut_-_google_art_project.jpg)

Honey, what’s our credit score? [PD]Wikimedia

Why? So many possible reasons. People who care about efficiency are by definition long-term thinkers. They think about the future. They make plans.

But also, people with efficient homes have lower carrying costs. Because banks don’t yet consider carrying costs in such detail, banks don’t give buyers credit for the money a low heating bill puts in the owner’s pocket. So efficient-house buyers are “richer” than banks can conceive.

And efficient homes are more likely to be bought by people with flexible mindsets, who aren’t puzzled by freakishly small furnaces, multiple fuel sources, heat pumps, heat sinks, geothermal gizmology, thick walls, and other peculiarities of green building. Flexible thinkers are also more likely to find a creative way out of a financial crunch, according to me.

This jives, oddly enough, with a study I saw yesterday linking pro-environmental behavior with the personality facets, Openness to Experience, and Conscientiousness.

50 SHADES OF FHA

B&D, FHA style. wikimedia commons pd

Numbers are the least sexy part of real estate. But let me see what I can do here to pump up the excitement: $98 a month, that’s what Obama’s new mortgage change will mean to the average Portland home-buyer who’s hot for an FHA loan.

FHA loans do help people of limited means slip into comfortable homes. But these loans tend to be turgid with fees. Among the most rapacious of these is the “mortgage insurance premium.” Right now, that fee engorges the purchase cost of your house by 1.35%.

This may not sound like a huge hunk, but whip out your calculator. Actually, let’s ask my smokin’ hot pal Laura D’Andrea (laura@lendersnetwork.biz) to whip out her calculator: She’s a Portland mortgage originator, and would be the first to assure you that size does matter. Taking an average Portland home, here’s the impact of the sleeker, stripped-down mortgage insurance premium (MIP). For a $245,000 house:

With the minimum 3.5% down payment, under the current MIP rate, you’ll pay about $266 each month just for the MIP. But for that same loan approved after January 26, the MIP payment will be $98 less. Over the life of a 30-year loan, that’s $35,280 in your pocket.

That’s $35,280 you could spend buying the house you’re passionate about vs. the house your mother would choose for you.

Now, two things about the MIP still rub me the wrong way. With “conventional” loans, you can slip the sweaty grip of MIP once you’ve paid for 20% of the home. After all, the whole point of mortgage insurance is to make sure the lender can recover its money if you pull a one night stand–and if the home is worth 20% more than the loan balance, the lender should be safe.

But FHA plays rough. It’s going to squeeze you tight for the entire life of the loan. So go ahead and take a tumble with this enticing new MIP. But keep that safe word on the tip of your tongue: Refinance!