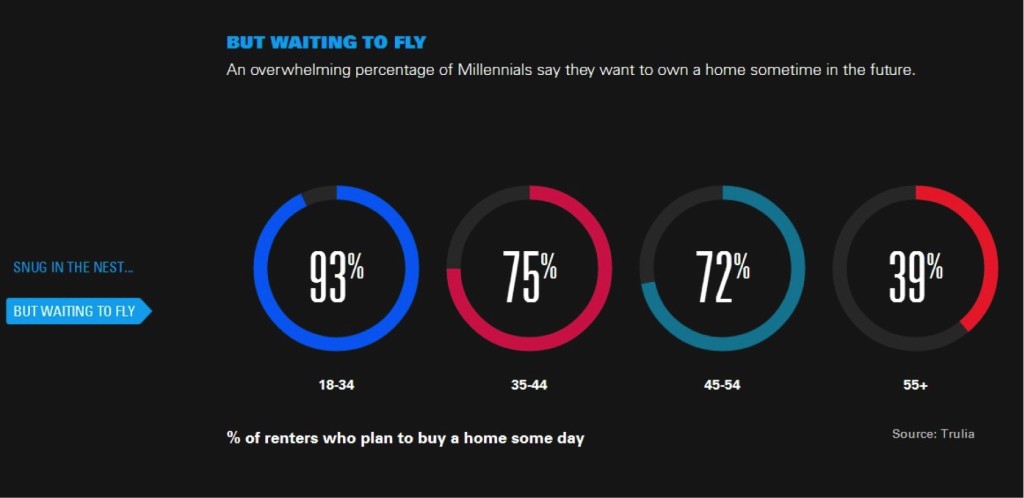

Art: trulia

I simply don’t know what to make of this. Every young person in America apparently wants to own a home. And very few older people do.

This Trulia survey of current renters suggests that the burning desire for ownership cools inexorably under the chill wind of age and experience. Or it suggests something else. I’m quite curious about it. But I’m most curious about these Millennials being all nesty and optimistic. It actually fits my experience with them as real estate clients.

These people were supposed to be sway-backed under the burden of debt, and dismal-eyed about their employment prospects. What went wrong? Well, they’re also considered a conscientious and idealistic batch of humans. And that’s what I see.

I’m excited about the communities they’re going to build.

![Wikimedia [PD]](https://geekrealtyblog.com/wp-content/uploads/2015/03/pieter_willem_frederick_wenning_south_african_1873-1921_narrow_street_malay_quarter_cape_town.jpg)

![Heat being heat. [PD] Wikimedia](https://geekrealtyblog.com/wp-content/uploads/2015/02/800px-american_school_-_the_burning_of_the_harbor_masters_house_honolulu_oil_on_panel_1852_honolulu_academy_of_arts.jpg)

![Honey, what's our credit score? [PD]Wikimedia](https://geekrealtyblog.com/wp-content/uploads/2015/01/agostino_brunias_-_a_leeward_islands_carib_family_outside_a_hut_-_google_art_project.jpg)